The 2026 financial landscape is defined by the full implementation of SECURE Act 2.0 provisions and the critical junction of the Tax Cuts and Jobs Act (TCJA) sunset. With the Federal Estate Tax Exemption reaching a peak of 15millionperindividual(15 millionperindividual (30 million for married couples) and the introduction of enhanced $11,250 catch-up contributions for specific age cohorts, the window for high-net-worth (HNW) optimization is narrow. This guide serves as the definitive technical manual for Holistic Financial Lifecycle Management, providing the mathematical and legislative framework required to navigate the current fiscal epoch.

What is the Definition of Financial Planning in a Holistic Lifecycle Context?

Financial planning is the mathematical synchronization of cash flow, asset allocation, and tax liabilities across a human lifespan. It functions as a structured lifecycle management system designed to mitigate sequence of returns risk while maximizing the net-present value of a multi-generational estate through rigorous quantitative analysis.

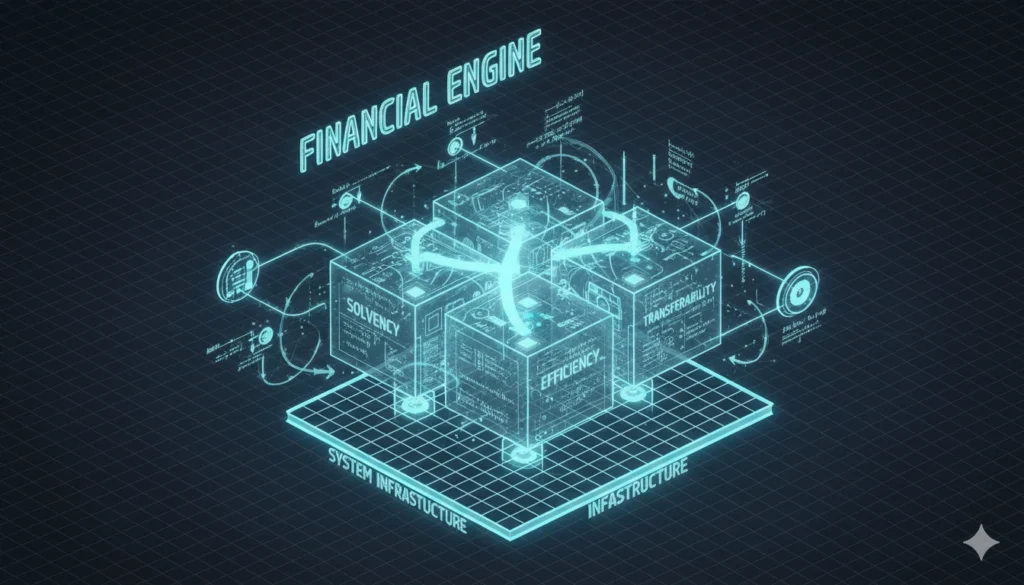

Financial planning is not a qualitative “goal-setting” exercise; it is an engineering discipline applied to capital. The core entity is the Financial Plan, which possesses three primary attributes: Solvency, Efficiency, and Transferability.

- Solvency: The maintenance of a positive net worth through the alignment of assets (EAV: Liquid, Illiquid, Deferred) against liabilities (EAV: Short-term, Long-term, Contingent).

- Efficiency: The optimization of the Internal Rate of Return (IRR) by minimizing friction costs, specifically taxes (marginal and capital gains) and management fees.

- Transferability: The structural capacity to move wealth between entities (e.g., from an individual to an Irrevocable Trust) with minimal leakage.

In 2026, the Fiduciary Standard is the baseline value for all professional advisory engagements. A fiduciary must legally prioritize the client’s interest, eliminating the conflict of interest inherent in commission-based “broker-dealer” models. The roadmap follows a strict hierarchy: Cash Flow Foundation → Tax-Advantaged Architecture → Risk Mitigation → Legacy Engineering.

How Does Cash Flow and Liquidity Management Prevent Capital Erosion?

Liquidity management minimizes the opportunity cost of idle cash by utilizing high-yield sweep accounts and laddered short-term instruments. It ensures immediate capital availability for opportunistic rebalancing while maintaining a cash-reserve buffer that prevents the forced liquidation of depreciated assets during market volatility.

The central entity here is Liquidity, and its primary value is its “Option Value.” Holding excess cash in a standard checking account results in a negative real return when adjusted for inflation.

The Opportunity Cost of Idle Cash

In the 2026 interest rate environment, “Idle Cash” is defined as any capital exceeding the 6-month operational expense threshold that is not yielding at least the 13-week Treasury Bill rate.

- High-Yield Sweep Accounts: These entities automatically move excess cash into higher-interest vehicles (typically money market funds or FDIC-insured clusters).

- The 2026 Solvency Ratio: A healthy lifecycle plan requires a Liquidity Ratio of 2.0 or higher, where liquid assets are double the current liabilities due within 12 months.

Cash Flow Synchronization

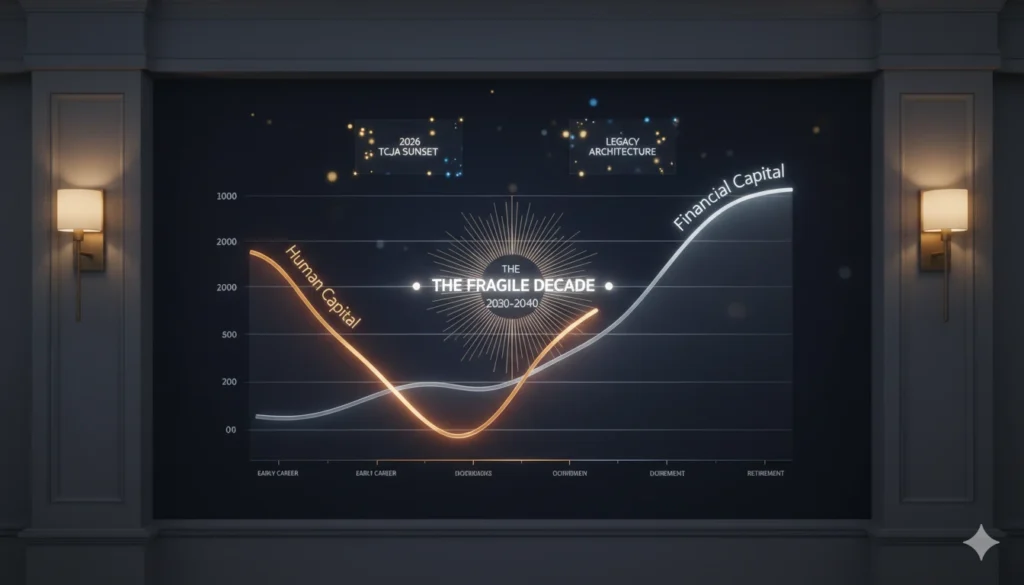

Synchronization involves aligning the “Inflow” (Salary, Dividends, RMDs) with the “Outflow” (Fixed Costs, Discretionary Spend, Taxes). If the synchronization fails, the investor incurs Sequence of Returns Risk, particularly in the five years preceding and following retirement. The 2026 protocol for high-earners mandates the use of Automated Treasury Ladders to capture yield while maintaining 30-day liquidity windows.

Which Tax-Advantaged Architectures Optimize Capital Retention in 2026?

Capital retention is optimized through the strategic use of Roth conversions, tax-loss harvesting, and the exploitation of the step-up in basis. These mechanisms shift tax liabilities from high-marginal-bracket years to lower-bracket periods, effectively increasing the total internal rate of return on the portfolio.

The 2026 tax code necessitates a “Tri-Bucket Strategy“: Taxable (Brokerage), Tax-Deferred (Traditional 401k/IRA), and Tax-Free (Roth/HSA).

The 2026 Contribution Landscape

The following values are non-negotiable for 2026 tax planning:

- 401(k) Contribution Limit: $24,500.

- IRA Contribution Limit: $7,500.

- HSA Contribution Limit: $4,300 (Individual) / $8,550 (Family).

Roth Conversion and Deferral

The attribute of “Tax-Free Growth” makes the Roth IRA the most valuable entity in the lifecycle. In 2026, high-earners (those with MAGI exceeding $145,000, indexed) must note that all catch-up contributions to employer-sponsored plans are mandated as Roth (after-tax).

Tax-Loss Harvesting (TLH): This is the process of selling securities at a loss to offset capital gains and up to $3,000 of ordinary income. In 2026, TLH must be automated to capture “intra-month” volatility. The value of TLH is the “Tax Alpha” generated, which often ranges from 0.50% to 1.10% in annual net returns.

What Risk Mitigation and Asset Protection Entities are Required for HNW Individuals?

Essential asset protection entities include Irrevocable Trusts, Umbrella Insurance policies, and Qualified Longevity Annuity Contracts (QLACs). These structures insulate personal wealth from litigation, provide longevity insurance against outliving capital, and facilitate the seamless transfer of assets outside the probate process.

The Umbrella Insurance Entity

Umbrella Insurance provides liability coverage above existing auto and homeowners’ policies.

- Attribute: Broad-form coverage.

- Value: For a household with $10M in assets, a $10M Umbrella policy is the mandatory baseline. This protects against “Judgment Risk,” which can liquidate decades of financial planning in a single legal action.

Irrevocable Trusts as Defense

Irrevocable Trusts (e.g., Spousal Lifetime Access Trusts or SLATs) remove assets from the grantor’s taxable estate.

- Attribute: Asset Segregation.

- Value: By transferring assets into an Irrevocable Trust in 2026, the grantor “locks in” the $15M exemption before the scheduled sunset at the end of 2025 (or future legislative changes). This entity provides Statutory Protection from creditors, as the grantor no longer “owns” the assets.

Risk Mitigation through QLACs

The Qualified Longevity Annuity Contract (QLAC) is an entity designed to mitigate “Longevity Risk.”

- 2026 Rule: Investors can allocate up to $200,000 from a traditional IRA into a QLAC.

- Benefit: These funds are excluded from Required Minimum Distribution (RMD) calculations, deferring taxes while guaranteeing an income stream starting at age 85.

How Do the 2026 SECURE Act 2.0 Provisions Change Retirement Strategy?

The 2026 provisions introduce a $11,250 catch-up contribution for participants aged 60–63 and mandate Roth-only catch-ups for high-earners. These updates require a pivot toward post-tax accumulation to hedge against future tax rate hikes and optimize the estate’s tax-free footprint.

The SECURE Act 2.0 (and its 2026 implementation phases) fundamentally altered the Retirement System entity.

The Age 60–63 Catch-Up Provision

For the tax year 2026, the catch-up limit for employees aged 60, 61, 62, and 63 is increased to the greater of $11,250 or 150% of the standard catch-up limit. This is a “Targeted Accumulation Window.”

- Condition: If the participant’s prior-year compensation exceeded $145,000, this $11,250 must be directed to a Roth account.

The $15M Estate Tax Exemption (2026 Status)

The Federal Estate Tax Exemption for 2026 stands at $15M for individuals and $30M for married couples.

- Strategic Imperative: Any estate exceeding $30M must utilize Gifting Strategies (using the Unified Gift/Estate Tax Credit) to move appreciating assets out of the estate.

- Step-up in Basis: This attribute allows heirs to inherit assets at their fair market value at the date of death, effectively eliminating the capital gains tax on the appreciation occurred during the decedent’s lifetime. Financial planning in 2026 prioritizes holding highly appreciated assets until death to capture this “Tax Reset.”

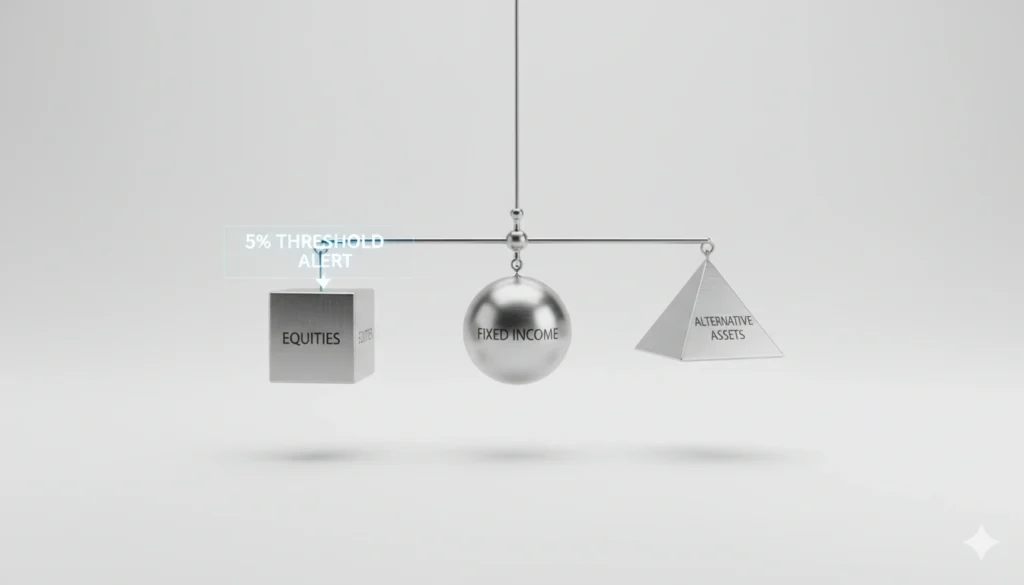

Why is Asset Allocation the Primary Driver of Portfolio Variance?

Asset allocation is the systematic distribution of capital across non-correlated asset classes, including equities, fixed income, real estate, and private credit. It accounts for over 90% of a portfolio’s return volatility, making individual security selection a secondary attribute of wealth management.

Rebalancing Thresholds

A static allocation degrades over time as one asset class outperforms another.

- The 5% Rule: In 2026, the standard rebalancing protocol triggers when any major asset class deviates by 5% or more from its target weighting.

- Direct Indexing: For HNW clients, Direct Indexing is the preferred entity. It allows for the ownership of individual stocks within an index, facilitating “Granular Tax-Loss Harvesting” that is impossible with a standard ETF.

Alternative Assets and Correlation

Holistic planning in 2026 requires exposure to Alternative Investments (Private Equity, Private Credit).

- Attribute: Low correlation to public markets.

- Value: Adding a 10-15% allocation to Private Credit provides a yield premium (Illiquidity Premium) that acts as a buffer against equity market “Drawdowns.”

Executive Synthesis

Holistic Financial Lifecycle Management in 2026 is a data-driven mandate. The synchronization of the 24,500401(k)limit∗∗,the∗∗24,500401(k)limit∗∗,the∗∗

11,250 specialized catch-up, and the $15M estate exemption requires a transition from passive “savings” to active “financial engineering.”

Core Directives for 2026:

- Maximize Roth Exposure: Given the mandatory Roth catch-ups for high-earners, prioritize tax-free growth to hedge against the 2026+ tax environment.

- Execute Estate Transfers: Utilize the $30M joint exemption before any potential legislative sunset or compression.

- Optimize Liquidity: Employ High-Yield Sweep Accounts to ensure cash reserves yield a positive real return.

- Implement Defensive Structures: Deploy Irrevocable Trusts and Umbrella Insurance to insulate the estate from external liabilities.

The complexity of the 2026 regulatory environment dictates that “hedging” is a failure of strategy. Successful lifecycle management relies on Declarative Certainty: executing specific mathematical protocols against known legislative variables to ensure the preservation and growth of multi-generational capital.