Life-stage planning is the strategic synchronization of financial resources with biological and economic milestones. It is an engineering discipline that manages the transition between two primary asset classes: Human Capital and Financial Capital. Human Capital represents the net present value (NPV) of an individual’s future labor earnings, while Financial Capital comprises the tangible assets accumulated over time. In the 2026 fiscal environment—characterized by the sunsetting of the Tax Cuts and Jobs Act (TCJA) and the maturation of SECURE Act 2.0 provisions—the objective of life-stage planning is to maximize Total Wealth through proactive tax-alpha generation, liability-driven investing, and rigorous risk mitigation.

Total Wealth management requires an intertemporal approach, accounting for the depletion of Human Capital as an individual ages and the corresponding necessity to build a robust portfolio of Financial Capital to fund the Decumulation Phase. Failure to synchronize these capitals results in structural solvency risks or inefficient wealth transfer.

What are the 2026 IRA Contribution Limits for the Accumulation Phase?

The 2026 Individual Retirement Account (IRA) contribution limit is $7,500 for individuals under age 50. This limit applies to both Traditional and Roth IRAs, provided the taxpayer possesses earned income. Individuals aged 50 and older may contribute an additional $1,000.

Section 1: The Accumulation Phase (Ages 22–35) – The Optimization of Human Capital

The Accumulation Phase is defined by the dominance of Human Capital. At age 22, an individual’s Financial Capital is typically negligible, while their Human Capital is at its theoretical peak. The strategic objective is the conversion of labor income into compounding assets with maximum tax efficiency.

The HSA as a Triple-Tax-Advantaged Vehicle

In 2026, the Health Savings Account (HSA) is the most efficient entity for long-term capital growth. Its attributes include:

- Tax-Deductible Contributions: Reducing current-year taxable income.

- Tax-Deferred Growth: Eliminating drag from capital gains or dividends.

- Tax-Free Withdrawals: When utilized for qualified medical expenses.

For HNW individuals in this phase, the HSA must be treated as a “stealth IRA.” By paying medical expenses out-of-pocket and allowing the HSA to remain invested in equities, the investor captures decades of tax-free compounding.

Roth Conversion Math and Early Career Optimization

Low-earning years at the start of the Accumulation Phase represent a unique window for Roth Conversions. Tax-alpha is generated by paying taxes at lower marginal rates (e.g., 10% or 12%) to ensure that the future value of the asset is entirely exempt from taxation during the Decumulation Phase. This hedges against “Legislative Risk”—the high probability that tax rates will be significantly higher 40 years in the future.

Disability Insurance as Human Capital Protection

The primary risk in this phase is the “Total Loss of Human Capital” via disability. A high-limit, “Own-Occupation” disability insurance policy is mandatory. Unlike “Any-Occupation” policies, an Own-Occupation rider ensures the payout triggers if the individual cannot perform the specific duties of their high-specialty profession, preserving the NPV of their future earnings.

Section 2: The Complexity Phase (Ages 35–55) – Risk Mitigation & Tax Efficiency

The Complexity Phase marks the “Sandwich Generation” era, where an individual simultaneously manages the financial needs of aging parents and dependent children. This phase requires the transition from simple accumulation to complex Tax-Advantaged Architecture.

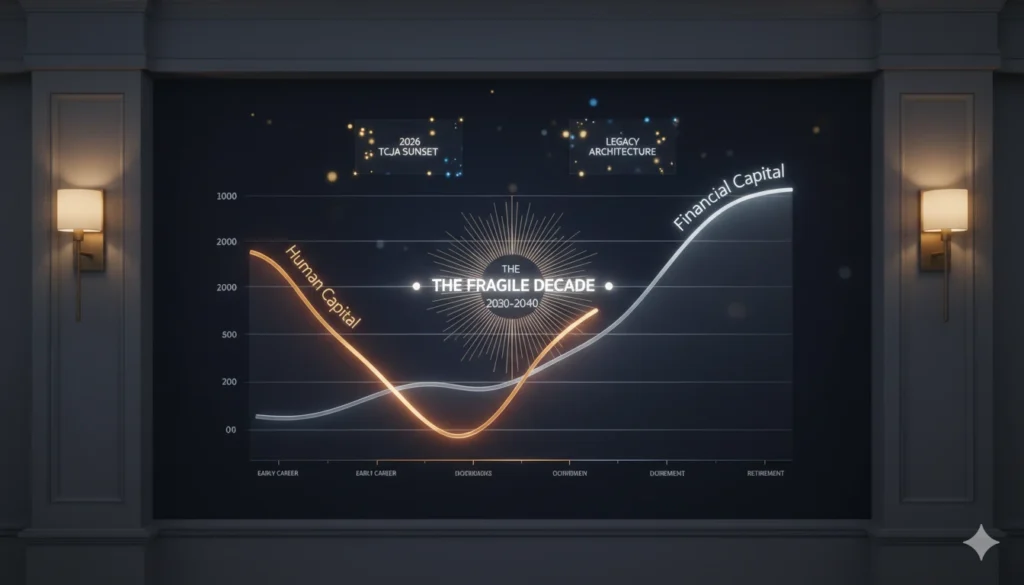

The 2026 TCJA Sunset Pivot

The most critical variable in 2026 is the scheduled sunset of the Tax Cuts and Jobs Act. This event will trigger:

- A return of the top individual income tax rate to 39.6%.

- The halving of the Unified Gift and Estate Tax Exemption (from approximately $14 million per individual to roughly $7 million, inflation-adjusted).

- The expiration of the Section 199A Qualified Business Income (QBI) deduction.

Lifecycle planning during these years necessitates a pivot. High-earners must maximize Defined Contribution and Defined Benefit plan participation to shield income from the rising 39.6% bracket. For business owners, the implementation of a Cash Balance Plan allows for annual contributions exceeding $200,000, significantly reducing the effective tax rate.

Education Funding and the 529-to-Roth Pipeline

Managing 529 Plan contributions is an exercise in intergenerational wealth transfer. SECURE Act 2.0 allows for the rollover of up to $35,000 (lifetime limit) from a 529 plan to a Roth IRA for the beneficiary, provided the account has been open for 15 years. This eliminates the “Overfunding Risk” associated with 529s and ensures that excess educational capital remains a tax-free asset.

Asset Protection and Umbrella Insurance

As Financial Capital grows, “Judgment Risk” increases. Umbrella Insurance is the primary entity for risk mitigation in this phase. A policy providing $5 million to $10 million in excess liability coverage is a baseline requirement for HNW households to protect the brokerage and real estate assets that constitute their net worth.

Section 3: The Pre-Retirement Phase (Ages 55–65) – Addressing Sequence Risk

The Pre-Retirement Phase is the “Fragile Decade.” It is the five years before and five years after the cessation of Human Capital earnings. The primary threat is Sequence of Returns Risk—the danger of a market downturn occurring during the early years of withdrawals, which mathematically compromises the portfolio’s longevity.

SECURE Act 2.0 Catch-Up Provisions (2026 Update)

In 2026, the legislative landscape offers a unique accumulation window. For participants aged 60 to 63, the 401(k)/403(b) catch-up limit is increased to the greater of $11,250 or 150% of the standard catch-up limit. However, high-earners (those with compensation exceeding $145,000 in the prior year) are mandated to make these catch-up contributions to a Roth account. This forces a transition toward tax-free asset buckets at the exact moment the individual is nearing their highest net worth.

Bond Ladders and Liability-Driven Investing (LDI)

To mitigate sequence risk, the portfolio must shift toward a Bond Ladder or a “Bucket Strategy.”

- Bucket 1 (Liquidity): 2–3 years of living expenses in cash and T-bills.

- Bucket 2 (Stability): 5–7 years of expenses in laddered investment-grade corporate bonds or TIPs.

- Bucket 3 (Growth): Diversified equities intended for use in years 10+.

By using an LDI approach, the retiree is never forced to sell equities during a bear market to fund monthly cash flow.

Section 4: The Decumulation Phase (Ages 65+) – Longevity and RMD Management

Decumulation is the process of spending down assets while navigating the complexities of the U.S. tax code and the risk of outliving one’s capital.

Sustainable Withdrawal Rates and Dynamic Spending

The “4% Rule” is a static baseline, but modern lifecycle finance utilizes Dynamic Spending models. By adjusting withdrawals based on portfolio performance—specifically using “Guardrails”—a retiree can increase their initial withdrawal rate to 5% or 5.5% during bull markets while decreasing it during drawdowns to preserve the principal.

Required Minimum Distributions (RMDs) and QLACs

Under current law, RMDs begin at age 73 (moving to 75 in 2033). RMDs are a “Tax Bomb” for high-net-worth individuals, often pushing them into the highest marginal tax bracket and triggering Medicare Part B IRMAA Surcharges.

To mitigate this, the use of a Qualified Longevity Annuity Contract (QLAC) is required. In 2026, an individual can move up to $200,000 from an IRA into a QLAC. This capital is excluded from RMD calculations, and the annuity payments can be deferred until age 85, providing a hedge against “Extreme Longevity.”

The Table of Asset Allocation by Life Stage

| Life Stage | Primary Focus | Equity Allocation | Fixed Income / Cash | Alternative Assets |

| Accumulation | Human Capital Growth | 90% – 100% | 0% – 10% | 0% (High Beta) |

| Complexity | Tax Efficiency | 70% – 85% | 15% – 20% | 5% – 10% (Priv. Equity) |

| Pre-Retirement | Sequence Risk | 50% – 60% | 30% – 40% | 10% (Priv. Credit) |

| Decumulation | Cash Flow / RMDs | 30% – 50% | 40% – 50% | 10% – 20% (Income Alts) |

| Legacy | Wealth Transfer | 60% – 80% | 10% – 20% | 10% – 20% (Illiquid) |

Section 5: The Legacy Phase – Wealth Transfer and Philanthropy

The Legacy Phase focuses on the frictionless transfer of Financial Capital to the next generation or charitable entities.

The Step-Up in Basis and Estate Engineering

The most powerful entity in U.S. tax law is the Step-up in Basis. When an individual dies holding appreciated assets in a taxable brokerage account, the heirs’ cost basis is adjusted to the fair market value at the date of death. This eliminates the capital gains tax liability on decades of appreciation. Strategic life-stage planning involves spending down tax-deferred assets (IRAs) first while holding highly appreciated taxable assets until death.

Irrevocable Life Insurance Trusts (ILITs)

For estates exceeding the 2026 sunsetted exemption levels (~$7 million per person), an ILIT is necessary. The trust owns the life insurance policy, removing the death benefit from the taxable estate. This provides immediate liquidity to pay estate taxes, preventing the forced liquidation of family businesses or real estate holdings.

Donor-Advised Funds (DAFs) as Tax Arbitrage

A Donor-Advised Fund allows for the immediate tax deduction of a charitable gift while the actual distribution to charities occurs over time. In a high-income year (e.g., the sale of a business in the Complexity Phase), an individual can donate appreciated securities to a DAF, avoiding the 20% capital gains tax and receiving a deduction at the 37% or 39.6% ordinary income rate.

Executive Synthesis: The Lifecycle Mandate

Life-stage planning is a non-linear optimization problem. It requires the constant recalibration of asset location, tax-bracket management, and risk hedging. As Human Capital declines, the precision of Financial Capital management must increase. In the 2026 landscape, the primary driver of wealth preservation is not market timing, but the mastery of legislative changes and the strategic use of tax-advantaged entities. The Individual Life Cycle is a closed-loop system; efficiency in the early stages dictates the solvency of the latter. Proactive execution of the strategies outlined in this guide—from HSA optimization to ILIT implementation—is the only way to ensure the integrity of a multi-generational estate.